What did SFTR tell us about the European repo market in Q3 2023

Executive summary

The EU repo market

· Growth slowed to just over 4% (compared with H1) to record an average daily turnover of some EUR 2.6 trillion and 91,000 trades. The summer break meant that growth was back-loaded into September. The estimated average tenor was about 25 days, little changed from H1 and still lower than in 2022.

· Average end-week balances grew at the same rate as turnover to exceed EUR 11.7 trillion and 449,000 trades.

· CCP-cleared transactions continued to dominate EU repo but also continued to lose share, falling to an average 55% of turnover. There was also a fall in average end-week balances to 47%, although this is still much higher than in 2022.

· Trading Venues lost share to the OTC market, which continued to expand, reaching an average 39% of turnover at the expense of EU-based MICs, which took 51%. However, OTC activity suffered from a surge in activity in non-EU MICs in September. There was little change in shares of outstandings.

· There continued to be a migration in terms of counterparty locations of turnover (and to a lesser degree in outstandings) away from repos between EU counterparties (47%) towards transactions between EU and non-EU counterparties (53%).

The UK repo market

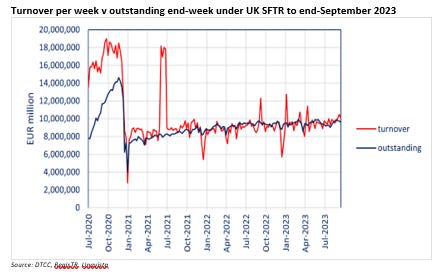

· Growth in the average daily turnover of repos in the UK slowed to just under 3% (compared with H1) but reached GBP 1,672 million = EUR 1,945 billion and almost 65,000 trades. Other than mini-peaks in activity in mid-August and early-September, Q3 was otherwise uneventful in terms of the published data.

· The average value of repos outstanding at end-week was GBP 8,139 million = EUR 9,468 million (-0.4%), while the average number of outstanding trades was about 423,000 (-10%).

· Compared to the EU repo market, the UK market continued to make less use of CCP-clearing. Moreover, that share declined further to 27% of turnover. CCP-cleared repo in the UK was even less significant in terms of end-week balances, averaging just 18%.

· The focus of UK repo remains OTC trading (56%) rather than Trading Venues. The share of UK MICs dropped to 10% and offshore MICs fell back to 29%. The share of UK MICs in end-week balances was even lower at 8%. But so were the shares of offshore MICs and the OTC market, as continued growth in the post-trade registration of OTC trades (XOFF) topped 9%.

· The average daily share of cross-border trades in turnover reached a new high of 83%, once again at the expense of domestic activity (16%). The pattern of changes in counterparty location was similar in terms of outstandings.

EU repo market

Look back to H1 2023

In the EU repo market, average daily turnover grew by almost 10.4% compared to 2022 to a record EUR 2.5 trillion and the average daily number of trades increased by 9.6% to 89,647 as higher interest rates, a sloped money market curve and reduced remuneration rates at the ECB for official deposits drew cash and new investors into repo.

On the other hand, average end-week outstandings over Q3 fell by 4.7% to EUR 11.2 trillion, while the average number of outstanding trades at end-week grew by 2.5% to 450,736, suggesting shorter average tenors, notwithstanding the higher term premium.

Q3 2023

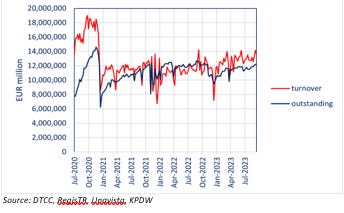

Turnover. The EU repo market saw growth in the average daily turnover in Q3 of +4.4% (compared with H1) to EUR 2,606 billion but the average number of new transactions was only slightly higher at 90,097 per day (+0.5%), increasing average trade size to EUR 28.9 million from EUR 27.8 million. After the end-June dip --- driven by seasonal window-dressing and the post-Credit Suisse/SVB focus on RWA --- turnover recovered, helped by demand off the back of TLTRO repayments, before falling back slightly and then flat-lining over the summer holiday period. Turnover was revived by the September bond futures expiry to peak in the week ending 22 September and possibly the last ECB rate hike, before the seasonal drop at end-quarter.

92.6% of new EU repos in Q3 were repurchase transactions.

Outstanding end-week balances trended up over Q3, peaking a little at month-ends. The average value over Q3 increased to EUR 11,735 billion (+4.4%) but the average number of transactions outstanding fell to 449,035 (-0.4%%), increasing average trade size to EUR 26.1 million from EUR 24.9 million.

91.2% of outstanding EU repos in Q3 were repurchase transactions.

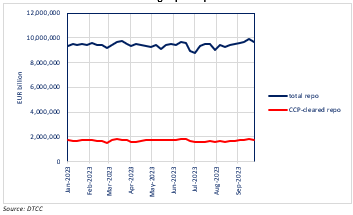

Turnover per week v end-week outstanding under EU SFTR to end-September 2023

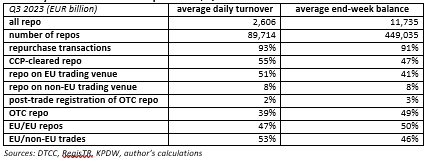

Summary statistics for the EU repo market, Q3 2023

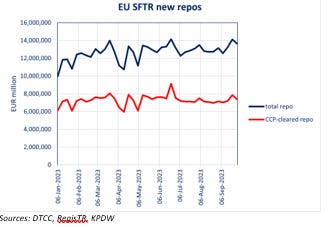

CCP-cleared repo turnover. The September bond futures delivery was the most notable event in an unexciting quarter for CCP-clearing in the EU market. Having peaked at 64.0% in the week ending 23 June, when futures-driven repo tend to mature, the average daily share of CCP-cleared repos fell to a low of 54.0% at end-July and then fluctuated within a band of 54-56%, averaging 55.4% over the quarter as a whole.

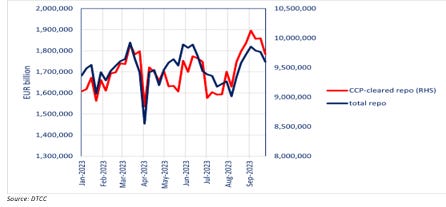

Total v CCP-cleared new repos reported weekly under EU SFTR, Q1-Q3 2023

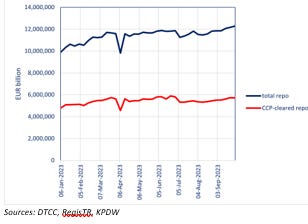

CCP-cleared outstanding repo. As with turnover, the share of outstanding CCP-cleared repos fell back sharply from mid-year. It then fluctuated between 46% and 47% before reviving slightly ahead of the September futures delivery. The average for the quarter was 46.6%, down from 48.3% in H1 but still well above the 41.1% seen in 2022.

Total v CCP-cleared outstanding repos reported end-week under EU SFTR, Q1-Q3 2023

Trading venues. The share of turnover of EU-based MICs declined in Q3, averaging 50.8% compared to 53.3% in H1, while OTC trading reinforced its share in the first two months of the quarter, averaging 39.4% compared with 37.7%. However, the share of OTC trading was dented in September by stronger turnover on non-EU MICs, which averaged 8.3% over the quarter compared to 7.3%.

In terms of the numbers of new transactions, the share of EU-based MICs fell to 57.6% in Q3 from 59.7% in H1, while the number of OTC trades increased to 34.3% from 32.8%, suggesting larger trades on EU MICs and smaller OTC trades. There was little change in shares of outstanding end-week balances.

Counterparty locations. There continued to be a flow of turnover away from repos between EU counterparties (to 46.8% in Q3 from 48.8% in H1) towards transactions between EU and non-EU counterparties as reported by the EU side (to 53.1% from 51.1%). This shift was more modest in terms of outstanding end-week balances. The volumes of business in the two segments now have a zero-sum relationship given the insignificance of reporting by non-EU counterparties. However, the quality of SFTR counterparty data remains suspect.

Average tenor. The normalised ratio of the number of outstanding repos at end-week over Q3 to the number of new repos per week --- which is a rough and ready measure of average tenor --- was almost25 days (also 25 days for repurchase transactions but 22 days for buy/sell-backs) compared with 25 days in H1 and 27 days over 2022. There is no obvious sign in the published data of longer trades seeking to exploit the term premium in the yield curve.

The estimated average tenor of CCP-cleared repo was 16 days. EEA MICs averaged 16 days, non-EEA MICs 27 days and OTC repo 37 days. Trades involving EEA reporting parties were 23-25 days and non-EEA reporting parties 91-130 days. Only the latter has been lengthening. However, these are not precise estimates (eg the CCP-cleared tenor looks too long) and the relative size of the numbers and changes are probably more informative than the absolute levels.

UK repo market

H1 2023

Average daily turnover in the UK repo market in the first-half of 2023 was GBP 1,656 = EUR 1,892 billion (+5.9% compared to 2022). The average number of new transactions was 63,819 per day (+24.1%).

The average value of repos outstanding at end-week over the first semester was GBP 11,069 = EUR 9,500 billion (+2.9%). The average number of transactions outstanding was 461,521 (+11.5%).

Like the EU repo market, the UK market benefited from a flow of cash and new investors drawn into repo by higher interest rates and a sloped money market curve.

Q3 2023

Turnover. The average daily turnover of repos in the UK reached GBP 1,672 million = EUR 1,945 billion in Q3 (+2.8% compared to H1). The average number of new transactions increased to 64,886 per day (+1.7%), which means that average new trade size was GBP 25.8 million = EUR 30.0 million, unchanged from H1 but down from GBP 29.6 million = EUR 34.7 million in 2022. In H1, there had been mini-peaks in turnover at each end-month but the mini-peaks in Q3 were at mid-August and early-September, possibly reflecting the importance being attached to the September bond futures delivery. Turnover in the UK market did not register the same end-June drop as in the EU, perhaps because window-dressing is less attractive in the UK, where LCR has to be calculated as a daily rather than monthly average.

97.1% of new UK repos in Q3 were repurchase transactions.

Outstanding. The average value of repos outstanding at end-week over Q3 was GBP 8,139 million = EUR 9,468 million (-0.4% compared to H1), while the average number of trades outstanding was 423,030 (-10.1%). Average outstanding trade size in Q3 was therefore GBP 19.3 million = EUR 22.4 million, up from GBP 18.0 million = EUR 20.6 million in H1. The larger average size of new trades compared to outstanding trades suggests that long-term repos were on average smaller than short-term trades.

95.7% of repos outstanding at end-week over Q3 were repurchase transactions.

Average tenor. The normalised ratio of the number of outstanding repos at end-week over Q3 to the number of new repos per week --- which is a rough and ready measure of average tenor --- was 32.6 days (32.7 days for repurchase transactions and 29.9 days for buy/sell-backs) compared with 36.2 days in H1 and 40.2 days over 2022.

Turnover per week v outstanding end-week under UK SFTR to end-September 2023

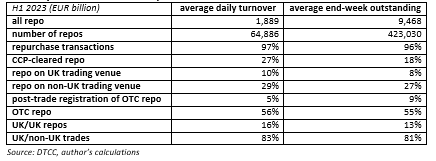

Summary statistics for the UK repo market, Q3 2023

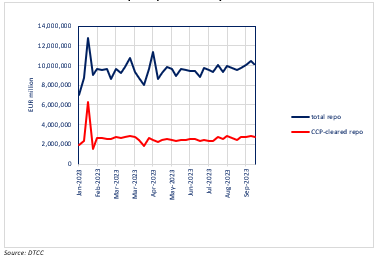

CCP-cleared turnover. CCP-cleared repo in the UK market continues to be much less significant than in the EU market, as shown by the distance between the total and CCP-cleared time series in the first chart below. The share of CCP-clearing in the UK was 26.8% in Q3 compared to 27.5% in H1 and 29.3% in 2022.

The second chart below, which aligns the total and CCP-cleared repo time series, shows that, despite its smaller share, UK CCP-cleared repo turnover is still a significant driver of the whole market, but less so in September.

Total v CCP-cleared new repos reported weekly under UK SFTR, Q1-Q3 2023

Total v CCP-cleared new repos reported weekly under UK SFTR, Q1-Q3 2023

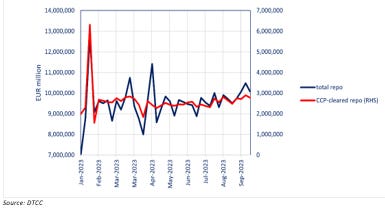

CCP-cleared outstanding repo. As shown in the next chart, the share of CCP-cleared repo in the UK was even less significant in terms of outstanding end-week balances than for turnover, averaging 18.3% in Q3.

Total and CCP-cleared outstanding repos reported end-week under UK SFTR, Q1-Q3 2023

The chart below, which aligns the total and CCP-cleared repo time series, shows that outstanding repo tends to drop off more sharply than total value at end-quarter, which is probably another bond futures effect. But there was a curiosity in May: an unseasonal run-off of CCP-cleared repos.

Total and CCP-cleared outstanding repos reported end-week under UK SFTR, Q1-Q3 2023

Trading venues. OTC repo reinforced its dominance of the UK market in Q3, taking 56.2% of turnover compared with 52.3% in H1 (+11.1%), having peaked at 58.5% in early September. The share of domestic MICs --- BrokerTec, eRepo, Tradeweb, GLMX, some voice-brokers plus some misreporting --- dropped to 10.2% from 10.9% in H1 and 13.7% in 2022. Offshore MICs fell back to 28.9% compared from 29.7% in H1 but remained higher than the share of 26.6% taken in 2022.

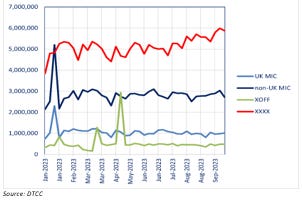

New repos by execution venue reported weekly under UK SFTR, Q1-Q3 2023

Source: DTCC

In terms of end-week outstanding balances, the share of domestic MICs was 8.4%, which was even lower than for turnover. This is modest. As domestic MICs are almost entirely for GBP repo, their 8.4% share of SFTR data can be compared with the 15% share taken by GBP cash and the 13% share taken by UK collateral in the last ICMA survey. However, the shares of offshore MICs and the OTC market also fell in Q3, although less so (to 27.3% and 54.9%, respectively). The reason was the large and growing share of the post-trade registration of OTC trades (XOFF). This reached 9.3%. It would appear that a lot of post-registered trades, particularly where they were registered on domestic MICs, were longer-term and so persisted into the end-week outstanding values. To that extent, the share of domestic MICs may have been understated.

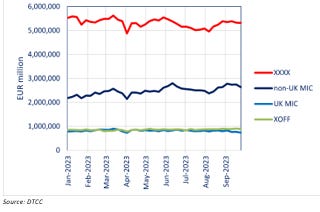

Outstanding repos by execution venue reported weekly under UK SFTR, Q1-Q3 2023

Counterparty locations. The average daily share of cross-border turnover reached a new high of 82.9% compared with 82.1% in H1, once again at

the expense of domestic activity (16.1% compared with 17.1%). The pattern of changes was similar in terms of outstandings, with the share of cross-border repos falling to 13.5% from 15.0% (however, some of the data are suspect).

Comparing the EU and UK

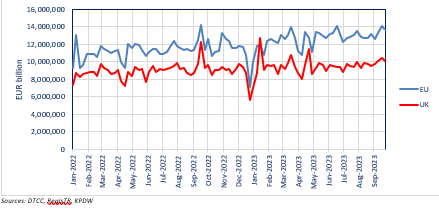

In Q3 2023, the total European repo market ex-EFTA, reported average daily turnover under the EU and UK SFTR regimes of EUR 4.551 trillion and 154,533 trades per day. The average end-week outstanding was EUR 21.203 trillion and 872,065 trades.

The difference in turnover between the EU and UK was higher in 2023 to date than in 2022. The gap widened in June, at the time of early TLTRO repayments but fell back slightly in Q3. The UK accounted for 45.9% of the combined turnover and 44.7% of average end-week balances, compared with 43.1% and 45.8% in H1 2023.

Total new repos reported weekly under UK and EU SFTR, 2022 to Q3 2023

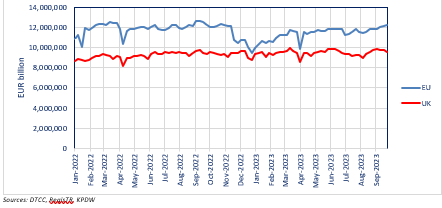

The difference in end-week balances between the EU and UK has been increasing over 2023 but remains lower than in 2022.

Total outstanding repos reported at end-week under UK and EU SFTR, 2022 to Q3 2023

Outstanding CCP-cleared repo has been growing significantly faster in the EU than in the UK over 2023. This is not the case in CCP-cleared turnover, suggesting more term repo being cleared in the EU (a trend claimed by Eurex GC Pooling).

The key statistical differences between the EU and UK markets, as measured by SFTR, are summarised in the table below. In essence, UK repos are less likely to be electronically-traded, CCP-cleared and with a domestic counterparty and more likely to be longer-term and larger.